Loading...

Correlation Part 1

Quiz by Robert

Tag the questions with any skills you have. Your dashboard will track each student's mastery of each skill.

The cost of inventory that is still on hand is called:

Another term for gross profit is:

Two accounts that appear on the financial statements of a merchandising company but are not needed bya service company are:

Sales revenue is based on the_________ of the inventory, while cost of goods sold is based on the___________ of the inventory.

Which is the CORRECT order of items to appear on the income statement?

A periodic inventory system:

The inventory system that uses computer software to keep a running record of the inventory on hand is the:

Which of the following statements about management accounting is FALSE?

An unfavorable variance occurs on a performance report when ___________________.

An favorable variance occurs on a performance report when ______________.

Who is the primary user of performance reports used to plan and control operations?

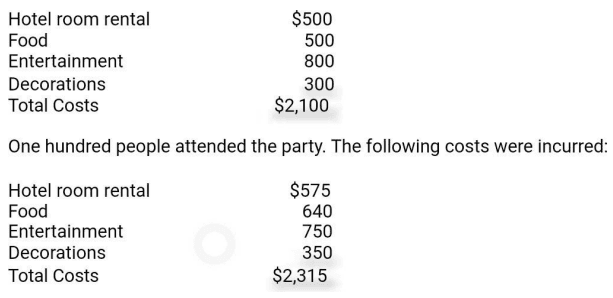

The Helium Company held a Christmas party. The company expected attendance of 100 people and prepared the following budget: What is the primary reason for the variance in total costs?

Which of the following statements, regarding the rules of debits and credits, is CORRECT?

The first step in recording a transaction in the journal is

The normal balance of an account:

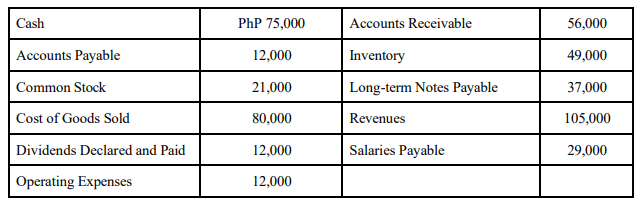

Think Company had the following accounts and balances at the end of the year. What are total liabilitiesat the end of the year?

Derry Company had the following accounts and balances at the end of the year. What is net income ornet loss for the year?

Millers Metalworks, Inc. has a total asset turnover of 2.5 and a net profit margin of 3.5%. The total debtratio for the firm is 50%. Calculate Millers’ return on equity.

Ortny Industries has an accounts receivable turnover ratio of 4.3. If Ortny has an accounts receivable balanceof $90,000, what is Ortny's average daily credit sales? You may use a 360- day year.

Managers may ____________ their budgeted costs or ___________their budgeted revenue to create a budget target that is easier to achieve.

Which of the following is the best indicator of management's effectiveness at managing the firm'sbalance sheet?

Storm King Associates has a total asset turnover ratio of 1.90 and a return on total assets of 7.20%.What is Storm King’s net profit margin?

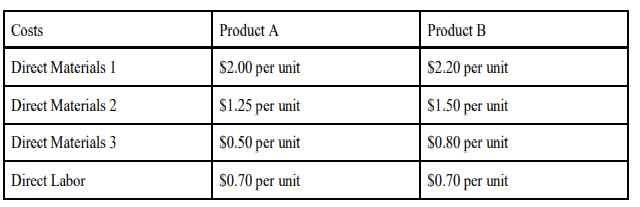

A company is trying to decide which product to manufacture. The following information is available: Which product cost is irrelevant to the decision?

When an engineer enters management, what is the most likely problem he finds difficult to acquire?

What management functions refers to the process of anticipating problems, analyzing them, estimating their likely impact and determining actions that will lead to the desired outcomes and goals?

Middle management level undertakes what planning activity?

What refers to situations in which moral reasons come into conflict, or in which the application of moral values is problematic?

What states the moral responsibilities of engineers as seen by the profession, and as represented by a professional society?

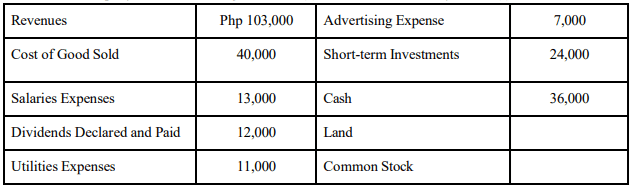

Sonia Company had the following account balances at the end of the first year of operations: What is the amount of net income or net loss for the year?

Heavy Load, Inc. has sales of $3,450,000, total assets of $1,240,000, and total liabilities of $275,000,which consist strictly of notes payable. The firm's operating profit margin is 16.1%, and it pays a 10% rate of interest on its notes payable. How much is the firm's time-interest-earned?

A company collects 60% of its sales during the month of sale, 30% one month after the sale and 10%two months after the sale. Expected sales are: $10,000 in August, $20,000 in September, $30,000 in October, and $40,000 in November. How much cash is expected to be collected in October?

Miller Metalworks had sales in November of $60,000, in December of $40,000, and in January of$80,000. Miller collects 40% of sales in the month of the sale and 60% one month after the sale. Calculate Miller's cash receipts for January.

Your firm is trying to determine its cash disbursements for the next two months (June and July). In any month, the firm makes purchases of 60% of that month's sales, which are paid the following month. In addition, the firm incurs the following costs every month and pays for them in the month the expenses are incurred: wages/salaries of $10,000, rent of $4,000, and miscellaneous cash expenses of $1,000.Depreciation amortized on a monthly basis is $2,000. June’s sales are expected to be $100,000, and July’s sales are expected to be $150,000. Cash disbursement for the month of July are expected to be:

Which of the following statements is true?

Given an accounts receivable turnover of 8 and annual credit sales of $362,000, the average collection period (360-day year) is:

Marshall Networks, Inc. has a total asset turnover of 2.5 and a net profit margin of 3.5%. The firm hasa return of equity of 17.5%. Calculate Marshall’s debt ratio.

Which of the following financial ratios is the best measure of the operating effectiveness of a firm’s management?

Kingsbury Associates has current assets as follows: Cash $3,000 Accounts receivable $4,500Inventories $8,000

Lorna T. Company has the following account. What is the ending balance in Retained Earnings?

Gerardo Company has the following accounts -(?) in the end of the first year of -(?) What are the total assets at the end of the first year?

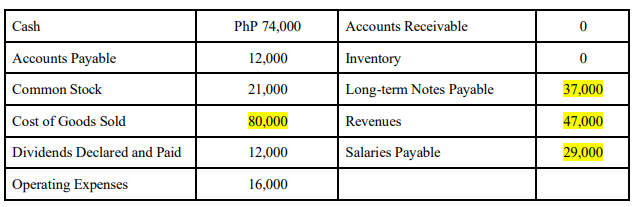

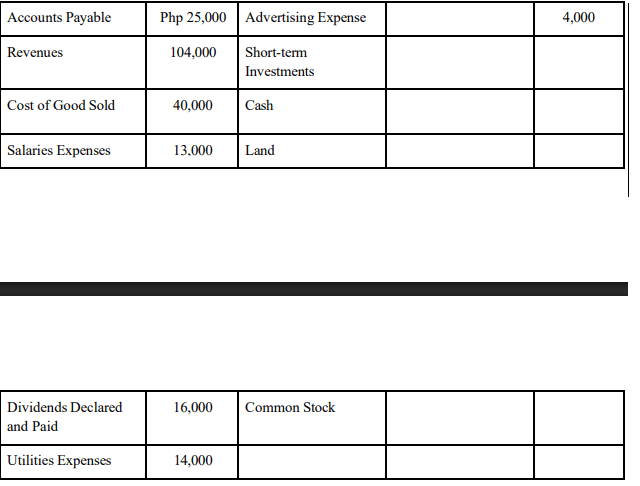

Linda Belangco opened a consulting firm, Belangco Consulting P.C. During its first month ofoperations, the following transactions were completed: At the end of the month total liabilities are:

I. Linda invested Php 30,000 in the business, which in turn issued common stock to her

II. The business purchased equipment on account for Php 63,000

III. The business provided consulting services on account, Php 13,000

IV. The business paid cash salaries to the receptionist, Php 2,000

V. The business received cash from a customer as payment on account Php 6,000

VI. The business borrowed Php 13,000 from the bank, issuing a note payable

A company completed the following transactions during the month of October:

I. Purchased office supplies on account, Php 5,600

II. Provided services for cash, Php 22,000

III. Provided services on account, Php 36,000

IV. Collected cash from a customer on account in the amount, Php 27,000

V. Paid the monthly rent of Php 3,800

What was the company's total revenue for the month?

A company completed the following transactions during the month of October:

I. Purchased office supplies on account, Php 4,800

II. Provided services for cash, Php 22,000

III. Provided services on account, Php 12,000

IV. Collected cash from a customer on account in the amount, Php 7,400

V. Paid the monthly rent of Php 18,000

What was the company's net income for the month?

Smith Corporation has current assets of $11,400, inventories of $4,000, and a current ratio of 2.6. What is Smith ‘s acid test (quick) ratio?

Water Works, Inc. has a current ratio of 1.33, current liabilities of $540,000, and inventory of $400,000.What is Water Works, Inc.’s quick ratio?

Which of the following ratios indicates how rapidly the firm’s credit accounts are being collected?

Smart and Smiley Incorporated has an average collection period of 74 days. What is the accountsreceivable turnover ratio for Smart and Smiley? You may use a 360-day year.

Billing’s Pit Corporation has an accounts receivable turnover ratio of 3.4. What is Billing’s PitCorporation’s average collection period?

Which of the following statements is true?

Snort and Smiley incorporated has a debt ratio of .42, noncurrent liabilities of $20,000, total assets of$70,000. What is snort and smiley's level of current liabilities?

. When performing a time study, the analyst convertsthe observed time into the time an "average" workerwould require working at an acceptable pace by using which of the following?

In stopwatch time study, adjusting the normal time by an allowance factor for normal delays andinterruptions results in the:

A job is expected to have a learning curve of 90%. The third unit required 16 hours. The twelfth unitshould take approximately how many hours?

A job has an 80% learning curve. The second unit required 12 hours to complete. Approximately howmany hours will be devoted to the first five units (including those already completed)?

A manager is trying to estimate the appropriate learning curve for a certain job. The manager notes thatthe first four units had a total time of 30 minutes. Which learning curve would yield approximately thisresult if the first unit took 10 minutes

A job had an observed time of 10 minutes, a performance rating of 0.90, and an allowance factor of20% of job time. Twenty-five cycles were timed. Standard time for the job in minutes is:

A job has a normal time of 12 minutes, a performance rating of 0.80, and an allowance factor of 20%of job time. The standard time for this job in minutes is:

Standard times derived from a firm’s historical data are known as:

Allowance percentages normally would not include:

A technique for estimating the proportion of time a worker spends on various activities is:

The technique which can be used to estimate the percentage of time a worker or piece of equipment isidle is known as:

Which sample proportion will require the largest number of work sampling observations?

What will be the effect on sample size in work sampling of increasing the permissible maximum error?

In work sampling, observations should be taken:

Design consideration for determining unadjustable work surface height

The optimum line of sight is roughly _____________ degrees below the horizontal

This is used to determine the range of adjustability for adjustable chairs

An anaerobic metabolism generates ___________which results in muscle fatigue during a staticmuscular activity.

It is the rate at which light energy is emitted in all directions from a light source measured in units of lumens

These are directed at reducing the noise intensity levels in the work environment

What is the combined noise level of two sounds of 86 and 96 decibels?

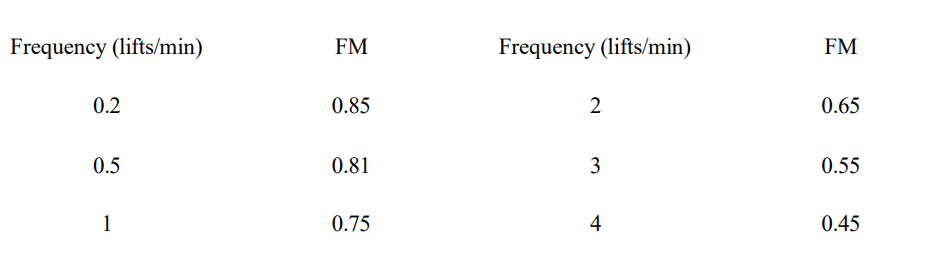

For 72-74. Many techniques developed for manufacturing industries can also be used for service industries.Consider sanitation workers who collect garbage bags left at the curbside for 8 hours a day. In a typical2-person team, one worker drives the truck, while the other walks the street, picking up the bags anddumping them into the truck (the lip of which is 50 inches from the ground). Typically the worker linesup the bag, picks it up by the tied top, twists 90° to lift it above the lip and drops it in. The height of thebag is 18 inches and the horizontal location of the load is 16 inches. Assume one garbage bag perhousehold (with a limit of 20 lbs to protect the workers), a distance of 70 feet between properties, and a walking speed of 3 mph (1 mile = 5280 feet).

The corresponding frequency multiplier for 8 hour period is shown below:

The frequency multiplier is:

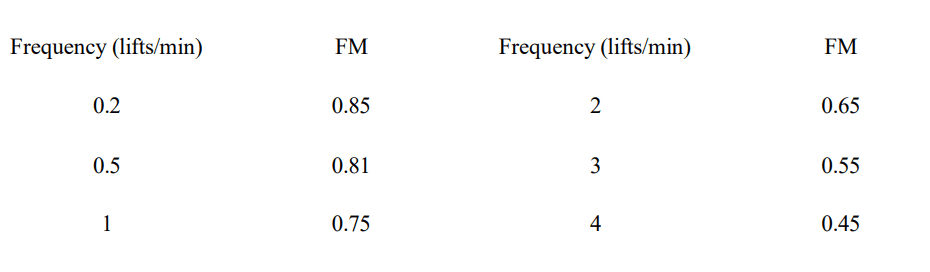

For 72-74. Many techniques developed for manufacturing industries can also be used for service industries.Consider sanitation workers who collect garbage bags left at the curbside for 8 hours a day. In a typical2-person team, one worker drives the truck, while the other walks the street, picking up the bags anddumping them into the truck (the lip of which is 50 inches from the ground). Typically the worker linesup the bag, picks it up by the tied top, twists 90° to lift it above the lip and drops it in. The height of thebag is 18 inches and the horizontal location of the load is 16 inches. Assume one garbage bag perhousehold (with a limit of 20 lbs to protect the workers), a distance of 70 feet between properties, and a walking speed of 3 mph (1 mile = 5280 feet).

The corresponding frequency multiplier for 8 hour period is shown below:

The horizontal multiplier is:

For 72-74. Many techniques developed for manufacturing industries can also be used for service industries.Consider sanitation workers who collect garbage bags left at the curbside for 8 hours a day. In a typical2-person team, one worker drives the truck, while the other walks the street, picking up the bags anddumping them into the truck (the lip of which is 50 inches from the ground). Typically the worker linesup the bag, picks it up by the tied top, twists 90° to lift it above the lip and drops it in. The height of thebag is 18 inches and the horizontal location of the load is 16 inches. Assume one garbage bag perhousehold (with a limit of 20 lbs to protect the workers), a distance of 70 feet between properties, and a walking speed of 3 mph (1 mile = 5280 feet).

The corresponding frequency multiplier for 8 hour period is shown below:

The lifting index (LI) is:

The Value of the horizontal multiplier when the load to be lifted is about 25 cm. In front of the operator is:

Which of the following is not an advantage of work sampling compared to stopwatch time study?

For #s 77-79. In an assembly process involving six distinct operations, it is necessary to produce 250 units per eight-hour day. The mean operation times are as follows:

7.56, 4.25, 12.11, 1.58, 3.72, and 8.44 minutes.

Determine the cycle time of the assembly process

For #s 77-79. In an assembly process involving six distinct operations, it is necessary to produce 250 units per eight-hour day. The mean operation times are as follows:

7.56, 4.25, 12.11, 1.58, 3.72, and 8.44 minutes.

How many operators would be required at 80% efficiency

For #s 77-79. In an assembly process involving six distinct operations, it is necessary to produce 250 units per eight-hour day. The mean operation times are as follows:

7.56, 4.25, 12.11, 1.58, 3.72, and 8.44 minutes.

How many operators will be utilized for the six operations?

Which of the following is not characteristic of time-based compensations plans?

What is the effect of an increase in the desired confidence level on the number of observations necessary in a time study?

What will be the effect on sample size in work sampling of increasing the permissible maximum error?

What is the standard time (ST) for this task if the employee worked at a twenty percent faster pace thanis average, and an allowance of twenty-five percent of the workday is used?

How many observations should be made if he wants to be 95.44 percent confident that the maximumerror in the observed time is one second?

How confident can the manager be that the true proportion of time spent mowing is between .45 and.55?

If the manager wants to be 95.44 percent confident that the true proportion of time spent mowing is within .02 (plus or minus) of the sample proportion. What should be her sample size?

Which of the following statements should not characterize an operations strategy toward the design of worksystems?

The design of work systems involves:

Methods analysis and motion study techniques develop which aspect of jobs?

A manufacturing operation is to be accomplished using 2 machines: X and Y. For a perfect balance, theratio between X to Y in a production line is 2:3. Machines X and Y produce sound at leves of 75 dBA and65 dBA, respectively. How much noise is produced by a well-balanced line?

Each sewing machine produces a noise of 70 dBA. What is the maximum number of such machinesthat can be put together in a room for the combined noise level to be tolerable for 8 hours?

Ms. Y is using green ink (R=0.30) to write on a yellow colored stationary (R=0.60). Light is providedby a 180 candela source positioned 1 yard above her writing table. What is the illumination on herstationary?

For 93-95. Fifty units of a special pump product are scheduled to be made for a Middle Eastern country to move wateracross the desert. A team of four workers will make the pumps, and they have already produced three units.Time records for the first unit were not kept; however, the second and third units took 15.0 hr and 13.4 hr,respectively. Using the Crawford learning curve model to solve this problem.

Determine the percent learning rate.

For 93-95. Fifty units of a special pump product are scheduled to be made for a Middle Eastern country to move wateracross the desert. A team of four workers will make the pumps, and they have already produced three units.Time records for the first unit were not kept; however, the second and third units took 15.0 hr and 13.4 hr,respectively. Using the Crawford learning curve model to solve this problem.

Determine the most likely time it took to do the first unit.

For 93-95. Fifty units of a special pump product are scheduled to be made for a Middle Eastern country to move wateracross the desert. A team of four workers will make the pumps, and they have already produced three units.Time records for the first unit were not kept; however, the second and third units took 15.0 hr and 13.4 hr,respectively. Using the Crawford learning curve model to solve this problem.

If the learning rate continues, how long it will take to complete the entire quantity of 50 units?

An analyst has observed 28 work cycles, for which the average cycle time was five minutes and theperformance rating was 1.05. Allowances for the department are 25 percent of job time. What standard time is appropriate for this job?

What number of observations would be required in a time study in order to obtain a 95 percentconfidence that the average time observed was no more than 0.6 minutes from the true mean, assuming astandard deviation of cycle time of 1.8 minutes?

A work sampling study was performed on the day-shift maintenance department in a power generatingstation. The day-shift consists of four repair persons, each of whom works independently to repairequipment when it breaks down. A total of 800 observations (200 observations per repair person) weretaken during a four‑week period (160 total hours of station operation). The observations were classifiedinto one of the following categories: (1) maintenance person repairing equipment, or (2) maintenanceperson idle. There were a total of 432 observations in category 1. It is known that 83 equipment repairswere made during the 4 weeks.

How many more observations would be required, if any, to be 90% confident that the true proportionof category 1 activity is within ± 0.03 of the proportion indicated by the observations?

It took exactly 10 hours to perform the first kidney transplant on a 100 percent learning curve. The second kidney transplant will take how many hours to perform?

The visual workplace includes

Kaninong buhok ito? (Surname only)

Sino ang napaiyak ni Hanna Claire na kinailangan bilhan ng Mcdo?

Sino ang nang iwan kay Ara Mae at nagpahagulgol sakanya ng mahabang panahon?

Sino ang ultimate bembang partner ni rerad?

Sino ang pinakamasarap sa paningin ni Hanna Claire na talagang naglalaway siya at naiisip niyang parang balut ito?