Tag the questions with any skills you have. Your dashboard will track each student's mastery of each skill.

Give this quiz to my class

Q 1/26

Score 0

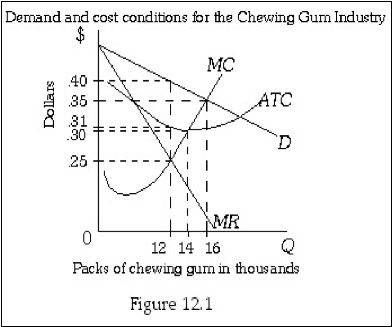

Refer to Figure. Six firms that produce chewing gum have formed a cartel. The cartel faces the market demand curve given by D. To maximize profits, the cartel should produce how many units at what price?

60

12000 @ $0.35

14000 @ $0.31

12000 @ $0.40

12000 @ $0.25

Q 2/26

Score 0

Which type of cost always increases immediately when output increases?

30

Marginal Cost

Variable Cost

Fixed Cost

Average Fixed Cost

26 questions

Q.

Refer to Figure. Six firms that produce chewing gum have formed a cartel. The cartel faces the market demand curve given by D. To maximize profits, the cartel should produce how many units at what price?

1

60 sec

Q.

Which type of cost always increases immediately when output increases?

2

30 sec

Q.

Diane's Donuts will begin selling donuts next week. Diane figures that the ingredients necessary to make donuts will cost $.05 per donut. She has paid $4,400 for the donut-making machinery and one year's rent. What will Diane's average total costs be if she sells 2,500 donuts in one week and then goes out of business?

3

120 sec

Q.

In the short run, the best policy for a perfectly competitive firm is to operate as long as price is greater than or equal to what?

4

20 sec

Q.

Equilibrium price is $19 in a perfectly competitive market. For a perfectly competitive firm, MR = MC at 120 units of output. At 120 units, ATC is $11, and AVC is $8. Should this firm shut down AND what is their profits or losses?

5

60 sec

Q.

Consider four types of markets: monopoly, perfect competition, oligopoly, and monopolistic competition. If they were ranked from the lowest number of firms to the largest number of firms, what would be the ranking?

6

45 sec

Q.

AG&T has a monopoly over local telephone service. If AG&T is producing where marginal revenue is greater than marginal cost, then how could the firm earn more profits?

7

45 sec

Q.

Which assumption in monopolistic competition drives each firm to zero economics profit?

8

30 sec

Q.

Assume that there is a single firm producing Go-Pros and the firm's specific demand curve is the same as the market demand curve. If a second firm that also produces devices similar to GoPros enters the market what will happen to the firm-specific demand curve of the original firm?

9

45 sec

Q.

When a profit-maximizing firm in monopolistic competition is producing its long-run equilibrium quantity, price will equal which type of cost?

10

30 sec

Q.

Which is Cost Curve "J"

11

20 sec

Q.

Refer to this table. What is the Marginal Cost of the second unit?

12

60 sec

Q.

What is the shape of a firm's demand curve in Perfect Competition

13

20 sec

Q.

What is this firm's profit maximizing level of output?

14

10 sec

Q.

Consider the following data: equilibrium price = $9, quantity of output produced = 1,000 units, average total cost = $8, and average variable cost $6. What is the Total Revenue and Total Fixed Cost?

15

60 sec

Q.

Assume a non-price discriminating monopolist can sell 15 units of a good for $3.00 each and can sell 16 units of that good for $ 2.85 each. What is the marginal revenue of the 16th unit?

16

60 sec

Q.

Given this table, what is the Marginal Revenue of the 2nd Unit?

17

45 sec

Q.

Which one of these is not a form of product differentiation?

18

30 sec

Q.

In the long-run, this monopolistically competitive firm would generate how much total revenue?

19

60 sec

Q.

Refer to this table. What is the Marginal Cost of the second unit?

20

120 sec

Q.

Which market structure guarantees long run profits?

21

20 sec

Q.

What would be the likely combined industry profit?

22

60 sec

Q.

An industry has only four firms, who have market shares of 45 percent, 25 percent, 20 percent, and 10 percent. What is the HHI?

23

60 sec

Q.

What type of good experiences a continuous decline in marginal cost?

24

20 sec

Q.

Compared to perfect competition, in the long run the monopolistic competitive firm produces where on the ATC curve?

25

30 sec

Q.

When marginal cost is higher than average cost, what is happening to average cost?